Laurus Labs has built a strong foundation on ARV generics and utilised the stable base to develop a thriving CDMO (Contract Development and Manufacturing Organisation) business. High-value business now accounts for 30 per cent of revenues in H1FY26 after gaining significant traction in the last two years compared to 19 per cent in FY21. The company is now entering another investment phase, focused on the CDMO segment, which should sustain the growth momentum and is adding specialised modalities for long-term growth.

The stock has priced in the growth sufficiently after rallying 75 per cent last year. The one-year forward valuations soared from 37 times earnings last year to 62 times now. Despite the premium valuations, we recommend investors hold the stock considering the growth outlook on the expanding CDMO platform.

CDMO small molecules

The CDMO segment now has 110 active projects, of which 15 are commercial supplies. These projects are largely with big- to medium-stage international pharma companies.

The segment reported 88 per cent year-on-year growth in H1FY26, following 49 per cent growth in FY25. Three factors aided this growth. Deliveries to mid- to late-stage programs, which are under evaluation, increased. These are higher volume compared to early-stage programs, which helps revenue growth. The company has increased share of deliveries to commercialised programs, which not only present a stable outlook on deliveries but also allow for volume growth as clients gain market penetration. Also, it has expanded the operations, which delivered growth for the segment.

The company has partnered with large pharma companies with pipeline depth across programs and is also setting up small molecule R&D teams to add early-stage projects. The company is also adding animal and crop science projects to the CDMO division, which should mature in the next two years.

CDMO large molecules

Laurus Labs is also expanding its large molecule (generally biologics, peptides or proteins) CDMO operations. The unit revenues are yet smaller compared to CDMO small molecule operations and has not scaled up to expectations.

But the company is doubling its fermentation capacity from 200 KL capacity in Bengaluru, with a new facility with 400 KL capacity in Visakhapatnam expected to be operational by CY26-end. This is in the first phase and should add more capacity in the remaining two phases. As per the company, the expansion in line with customer requirements and this provides revenue visibility to the segment.

The company has a proven capability in complex biologic projects. Its associate, ImmunoACT (an IIT Bombay incubated company), manufactures NexCAR19, which is a CAR-T cell therapy approved for treating relapsed/refractory B-cell lymphomas and leukaemia (blood cancers).

It is building capacity in cell and gene therapy projects. The company also has capability to produce integrated ADCs, which are the leading products in Immuno-oncology. ADCs or Anti Body Drug Conjugates involve a seeker, a toxin and a linker. The company specialises in the latter two and has also acquired a company for the same.

While fermentation-based revenues are more mid-term in nature (FY27 and beyond), ADCs, cell and gene therapy are longer-term capabilities. But this allows the company to present a one-stop shop for big pharma contract research outsourcing.

Generics

The generics segment consists of ARVs (Anti retro virals for HIV treatment) and non-ARV, which includes high potent oncology products.

The ARV segment of generics has been the main pillar for the company and is a stable business. The company, based on debottlenecked capacities and higher demand, has driven a strong growth of 20 per cent in the last three quarters. The segment should continue to deliver at the current revenue levels, as per the company.

The non-ARV segment is driven by CMO operations (contract manufacturing of APIs and intermediates) and the company’s own formulations for the US and Canada markets. The company is expanding the CMO oral capacity in Visakhapatnam and is developing a facility under a JV with KRKA (a European Pharma company). Under own formulations, it aims to have a leading presence in 15 molecules and is working towards the same.

Capital expansion

Laurus Labs is engaging in another round of high capex programme. The last capex round drove the diversification from generics with CDMO and the one prior to it added non-ARVs to the generics mix. This current endeavour will focus on expanding the CDMO operations for small and also large molecule segment along with adding capacity in generics and CMO segments.

With order visibility and customer demand, the small-molecule CDMO division will be the major beneficiary of the ₹5,000-crore expansion in Visakhapatnam. The expansion also includes the expansion of the fermentation capacities, as mentioned. This expansion is a five-year plan with an outlay of ₹1,000 crore or more for the next five years.

The company has also secured 532 acres in Visakhapatnam with plans to invest $600 million over eight years, apart from the above plans. It intends to fund the expansion with internal accruals and debt, if needed.

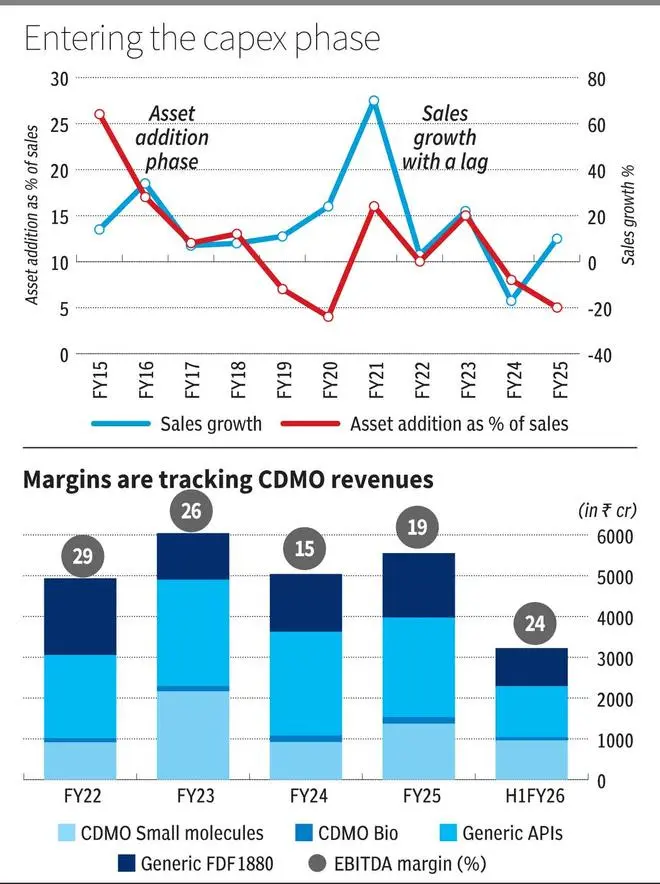

The company EBITDA margins have been volatile as the assets remain underutilised earlier. It reported an EBITDA margin of 24 per cent in H1FY26 as CDMO share of revenues increases. Its net debt to EBITDA stands at 2.5 times, as of March 2025.

Laurus Labs has revenue visibility backed by strong expansion plans in high-value CDMO segment along with specialty modalities of biologics CDMO. But with the stock trading at 62 times one-year forward earnings, valuations imply holding the stock and not adding fresh positions.

Published on December 6, 2025

{kind=link}