If Finance Minister Nirmala Sitharaman’s comment a few years back made one wonder if India Inc is like Hanuman, unaware of its own strength, and hence being over cautious when it comes to investing for growth, last week’s comment by Chief Economic Advisor Anantha Nageswaran makes one wonder if it is not more like Sugriva, who after being reinstated as king and enjoying its bounties, initially failed to fulfil his end of the deal and, hence, needed to be sent a stern message.

While speaking at a CII event the CEA made a strong statement when he said that the Indian private sector has found ‘enough reasons’ to remain cautious and risk averse by holding back investment decisions that could turn the strategic constraints the country faces into opportunities. Hard facts bear out this statement.

While there is no clear pact between the government and India Inc, since the time when a series of pro-investment measures were taken to revive animal spirits, starting with the pivotal corporate tax cuts in September 2019, the expectation was that industries would seize the opportunity.

Stark gap

But an analysis of data indicates that while India Inc’s market-cap, profit margins and bottomline have fattened nicely as a result of numerous government measures — corporate tax cuts, Covid stimulus, thrust on infrastructure, subsequent fiscal discipline, etc — its investments haven’t.

This inference is based on data of all companies that were part of the Nifty Total Market Index in FY19 and now, and after excluding financials (not a driver of capex). A total of 549 companies (referred to as India Inc) were considered for this analysis. Data was sourced from Bloomberg.

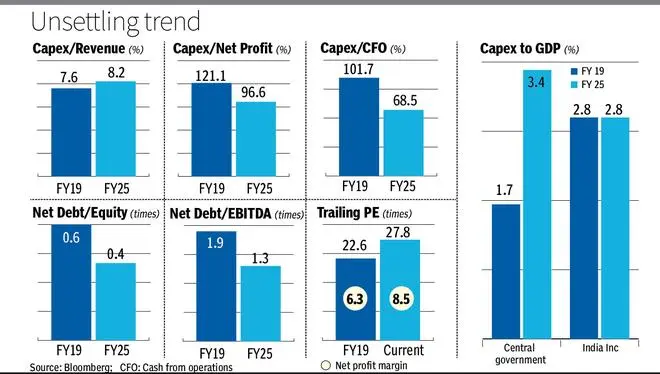

In FY19, the year when business sentiment was at its nadir due to various reasons including a series of disappointing GDP reports (hit a multi-year low in June Q of FY20), fear of tax terrorism, bank NPA problems, etc, India Inc invested around 8 per cent of its revenue, 121 per cent of its net profit and 102 per cent of cash from operations in capital expenditures or what can be termed as investing for the future.

However, in FY25, India Inc invested around a similar 8 per cent of revenues, a lower 97 per cent of net profit and much lower 69 per cent of cash from operations in capital expenditures. Net profit margin has increased from 6.3 per cent in FY19 to 8.5 per cent now — a sizeable 220 basis point surge. If financial companies are included the margins are even higher at 10 per cent now. Today, many Indian companies’ net profit margins across industries are much higher than their global peers.

Govt push

Reading these data together implies much of the benefits of improvement in margins and thereby profits, which stem from factors like corporate tax cuts, higher economic growth from government stimulus and capex thrust, have largely accrued only to shareholders so far. This can also be gauged from market capitalisation for these companies increasing by 204 per cent between FY19 and now while capex has increased only by around 75 per cent.

The caution in investing is also reflected in the stronger balance-sheet of India Inc. Between FY19 and FY25, net debt/equity for India Inc has improved from 0.55 times to 0.36 times now and net debt/EBITDA, too, has improved from 1.9 times to 1.3 times.

All put, this begets the question what is holding back investments today when balance-sheets, profit margins, business sentiment are much better than in FY19 and when unlimited opportunities in an AI and EV world beckon? A recent newsletter from PMS firm Spark Asia Impact Managers makes a sobering point — ‘there is not a single company in Nifty 50 which is IP-driven.’

Given the chorus of international and domestic corporate titans proclaiming this to be ‘India’s Decade,’ why has private investment lagged?

Is it lack of ‘need for ambition’, ‘need for risk taking and long term investing’ something the CEA highlighted is much warranted today? After all the world offers examples of many success stories from companies that were ambitious and seized the opportunity – like the world’s largest EV company BYD, which was only a maker of rechargeable batteries for mobile phones two decades ago. Even in the home turf we have an example of how Reliance Industries, a petrochemical player 15 years back, is today the largest telecom company and also one of the most notable telecom success stories globally. While such examples in India are rare, there is enough evidence that the long term vision from corporates can drive transformation. To be sure, there are few companies that are investing big today — like companies in the energy, power and metals space. But, in aggregate, the India Inc number is not encouraging.

Risk aversion

Here is another data point — government capex as percentage of GDP has doubled from 1.7 per cent in FY19 to 3.4 per cent now. What about India Inc? It was 2.8 per cent of GDP in FY19 and remains at 2.8 per cent in FY25.

In a capitalist economy, private sector is expected to be the engine of growth and not the government. As government commits to fiscal discipline, what the private sector decides to do from here will matter most for the country’s GDP growth than in previous years. Eventually, it will matter even more for India Inc’s shareholders. With valuation for the companies considered in this analysis at a trailing PE of 28 times today versus 23 times at end FY19, the earnings expectations are high. Innovation, long-term vision and risk taking are warranted even more to meet those expectations.

Published on November 22, 2025

{kind=link}