The stock of Kotak Mahindra Bank (KMB) had been in a time-wise correction since early 2021 until February this year, when the RBI lifted the embargo on the bank’s credit cards. It quickly gained 23 per cent from the lows of February to record an all-time-high price in April. Now, reacting to the Q1 FY26 earnings, the stock fell 7.4 per cent early last week and erased almost all gains since February.

Net profit for the bank declined 6.8 per cent. While rate cuts and the resultant pressure on margins do have their role here, what came as a surprise was elevated provisions and the management’s commentary on asset quality. Though stress in the microfinance (MFI) portfolio seems to have peaked and that in personal loans and credit cards plateaued, the bank is now seeing stress build up in the retail commercial vehicle (CV) segment as well. Consequently, slippages rose sequentially and the GNPA ratio, too, marginally rose 6 basis points (bps) to 1.48 per cent.

The stock now trades at a P/B ratio of 2.4x (consolidated), down from 2.7x before last week’s correction. Given that the stress segments only have a small share in the overall loan book and assuming that slippages and provisions will be contained in due course of time (as seen in cards and personal loans) with tighter underwriting norms, investors could factor in a higher RoA for FY26 than the 1.9 per cent (annualised) seen in Q1. This will be aided by the two levers for margin expansion, detailed later.

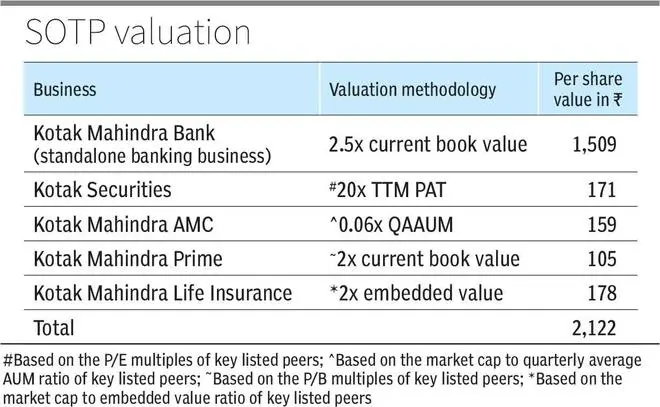

A conservative sum-of-the-parts valuation (at 2.56x consolidated book value per share) reveals a limited six per cent upside from current price. Investors willing to see through the bank’s near-term headwinds can accumulate on dips of 10 per cent or more, as the margin of safety is comfortable at those levels.

Though advances and deposits grew at a healthy 14 per cent and 14.6 per cent respectively year on year, net profit (standalone bank) declined 6.8 per cent. This was mainly due to higher provisions and a 32-bp sequential drop in NIM, which kept net interest income growth to just 6 per cent, despite healthy loan growth.

Pockets of trouble

Though stress has stabilised in personal loans and has plateaued in credit cards because of cautious underwriting, the MFI portfolio continued to trouble the bank. Credit cost (annualised) rose to 0.93 per cent, from 0.6 per cent for full-year FY25. This was largely due to the MFI portfolio. The bank is also seeing stress in the retail CV segment, the early signs of which were identified a couple quarters ago.

The management assesses that credit cost has peaked and will recede in the second half of the year. With the tighter underwriting measures that the bank has undertaken (including the shift in risk assessment from group level to individual level for MFI loans), the share of unsecured loans in the overall loan book has fallen from about 12 per cent, as of FY24, to 9.7 per cent currently.

Individually too, they make for a small part of the loan book. The share of MFI and credit card book are 1.3 per cent and 2.8 per cent. Personal loans (individual share unknown) are part of a larger segment, which includes business loans and consumer durable loans, and this segment accounts for 5.3 per cent. Similarly, retail CV loans are part of the ‘Commercial Vehicles, Construction Equipment loans’ segment, which makes up 9.4 per cent of the loan book.

The management is comfortable with how the newly originated accounts have behaved after the tighter underwriting and hence, are upbeat about growth in these segments, once macros settle down.

Margin levers

As for the other factor that drove profit down, the NIM declined 32 bps sequentially in Q1 to 4.65 per cent. This is higher than the decline of about 10 bps that HDFC Bank and ICICI Bank have seen. However, there are certain nuances here.

The bank has a floating rate book of around 60 per cent and in general, KMB takes three months to fully pass on rate cuts to the borrowers. While a large part of the rate cuts in February and April has been passed on, the transmission of the 50-bp cut in June will take place in Q2 and thus, NIM is expected to bottom out then (provided there are no more rate cuts). Further, unlike its larger peers, the bank can ramp up unsecured lending (where yields are higher) to shore up margin, when it feels comfortable doing so. This is the first lever.

The second lever is on the cost side. In Q1, the cost of funds declined 8 bps to 5.01 per cent, as the bank reduced interest rates on deposits. The cost of savings accounts, which account for 25 per cent of the total deposits, fell 47 bps sequentially to 3.32 per cent (KMB wants to take it down further to 2.5 per cent). If one were to apply the 25 per cent weight on the 47-bp decline to determine its effect on the overall cost of funds, the resultant figure itself accounts for a 12-bp decline in cost of funds. Of course, this is not an accurate estimate, as cost of funds encompasses interest incurred not just on deposits, but also on borrowings. But this gives a rough idea that the reduction in rates of term deposits is yet to take effect. With the average tenor of term deposits between 9 and 12 months, it can be said that much of the repricing can be expected to take place towards the tail end of the year.

Key monitorable

Considering the above factors, FY26 appears to be a turbulent one for the bank. While the above levers do exist, the real test lies in execution. Deposits need to be repriced without denting market share. Asset-quality stress must remain benign to ramp up high-yield products. Hence, investors who are in for the long game can accumulate the stock on dips of 10 per cent or more, while keeping a keen watch on how the pockets of trouble behave.

Published on August 2, 2025

{kind=link}