Investment in infrastructure and military isn’t straightforward in a country that often struggles to get things done.

Author of the article:

Published Apr 07, 2025 • 6 minute read

Article content

(Bloomberg) — German Chancellor-in-waiting Friedrich Merz has locked in political backing for a grand plan to ramp up investment in its infrastructure and military.

Article content

Article content

Now he needs to spend the money, and that’s not straightforward in a country that often struggles to get things done.

Time is of the essence: US President Donald Trump’s rush for peace in Ukraine and his disengagement on defense will quickly put the onus on Germany and Europe to take up the security mantle — a task Merz has already recognized as critical. And he knows too that the region’s biggest economy, already vulnerable to the White House’s trade protectionism, can’t afford yet more lost years.

Advertisement 2

Article content

But even after painstaking coalition talks conclude in coming weeks, Merz’s achievement of loosening budget rules to unleash a debt-fueled spending spree will face a gauntlet of extended scrutiny by lawmakers, followed by bureaucratic decision-making on its implementation, all slowed down by limited capacity.

The incoming chancellor must urgently transform the German state or else risk that the open fiscal floodgates produce more of a trickle than a deluge for much of his term. Failure could leave the country with an inadequate defense deterrent against Russia, facing yet more economic malaise, and could also cast a shadow over his push to contain the far-right AfD.

“This will take time,” said Werner Gatzer, a former deputy German finance minister who is now chairman of Deutsche Bahn’s supervisory board and part of a group advocating measures to streamline government. “The money is available now. The next step must be reforming the state itself.”

The cash hoard that will be at Germany’s disposal is commonly cited at as much as €1 trillion ($1.1 trillion). That comprises a special fund of €500 billion for infrastructure and then money for defense, no longer restricted by the country’s debt brake after Merz engineered constitutional changes requiring extra-large majorities of lawmakers.

Top Stories

Article content

Advertisement 3

Article content

A stagnant economy already made such investment desirable, but Europe’s defense weaknesses create even more of an imperative. Analysis of the Russian threat by military planners points to the need for a credible deterrent within five to seven years.

The kick start to prosperity from a spending spree could be significant. Deutsche Bank economists have raised their forecasts for economic growth in 2026 to 1.5% from 1%, reaching a pace of 2% in 2027. That’s in line with recent revisions from Goldman Sachs and Commerzbank.

“After many years of doom and gloom and in times of great uncertainty, the fiscal package can be a real game-changer for the sentiment in the economy,” Barclays chief economist Christian Keller said. “When companies and investors see opportunities, they usually seize them.”

But the money itself could be slow to arrive: the year may be drawing to a close by the time the infrastructure fund becomes law, and in common with other advanced economies, large German projects face drawn-out procurement, permitting and planning processes that often consume far more time than actual construction.

Advertisement 4

Article content

Implicit in the economic forecasts is a sluggish start to stimulus, only reaching its full impact in 2027 — when Merz’s term of up to four years passes its halfway point.

Deutsche Bank reckons the infrastructure spend will total €30 billion in 2026. It would then double to €60 billion in 2027 before falling back to €40 billion in 2028. It projects defense outlays to rise from €80 billion to €110 billion in 2026, reaching €150 billion in 2027.

That chimes with the timetable envisaged by Tammo Diemer, co-head of Germany’s finance agency that manages the country’s debt, who sees its requirements from capital markets rising only “gradually, year by year.”

Germany can move fast when necessary, with the most eminent recent example being the creation of liquid natural gas terminals in record time after Russia’s invasion of Ukraine endangered energy supplies.

That was a special case however, delivered under duress. The country is more used to multi-decade sagas, such as the construction of Berlin’s Brandenburg airport and the still-unfinished revamp of Stuttgart’s train station.

Advertisement 5

Article content

Recent spending has fallen short. In 2023, a staggering €76 billion — 16% of Germany’s total finance plan — went unused due to hindrances such as bureaucratic hurdles, supply bottlenecks and staff shortages. Areas focused on by Merz’s push have been particularly challenging.

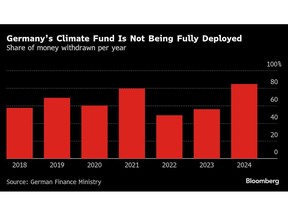

The government’s Climate and Transformation Fund, known as the KTF, which subsidizes projects like electric vehicle charging, has only disbursed about 65% on average in the past seven years. It will receive €100 billion of the planned €500 billion stimulus.

Germany’s €100 billion military fund, set up by current Chancellor Olaf Scholz’s coalition, is another example. While most of the money has been earmarked for weapon purchases, only a quarter of it has actually been disbursed in the past three years.

One problem there is a strict postwar regime that prohibits Germany’s arms industry from stockpiling weapons. Relaxing such restrictions may boost production, said Monika Schnitzer, chair of the country’s independent council of economic experts. She also reckons manufacturers such as Rheinmetall, Hensoldt and Diehl Defense could poach talent from the struggling automotive sector.

Advertisement 6

Article content

Labor shortages remain a widespread theme however, and with a large construction workforce needed for Germany’s infrastructure push from fixing bridges to renovating hospitals and schools, that might prove another brake on spending.

“If we look at the construction industry, it is running at full capacity at the moment,” said Ifo Institute President Clemens Fuest. “There are concerns that more money thrown at them will raise prices.”

What Bloomberg Economics Says…

“Germany’s economy is structurally weak, as it deals with a shift away from Chinese demand, higher energy costs and a faltering autos industry. Higher investment spending could significantly help address those challenges, smoothing the economic transition and boosting potential GDP by 2% in the long term.”

—Martin Ademmer, economist. For full note, click here

More flexible working hours and prioritizing digitalization in public infrastructure administration could help clear some bottlenecks, according to Stefan Kolev, Director of the Ludwig Erhard Forum for Economy and Society.

He and other economists including Fuest and Bundesbank President Joachim Nagel say the government mustn’t let up on growth-friendly reforms. Nagel, among other things, is urging labor market-oriented migration or incentivizing older people to work.

Advertisement 7

Article content

Gatzer, whose career in the finance ministry gave him unique insights into Germany’s bureaucracy, says the LNG success shows what to focus on: limiting appeals, overriding procedural processes and resisting lobbying pressure as well as protests.

“The new government has a heavy burden of responsibility to get this right,” said Ulrike Malmendier, a professor at the University of California who, like Schnitzer, is a member of the panel of economic experts. “Structural reforms need to follow.”

Social Democrat co-leader Lars Klingbeil — a frontrunner to be the next finance minister in the likely coalition with Merz’s CDU/CSU — last week pledged a “new spirit” to accelerate investment of the €500 billion of special funds.

“We must ensure that the money isn’t invested in Germany at the usual speed,” he told public broadcaster ZDF. “Everything shouldn’t have to be approved 20 times, planned 30 times, take umpteen years.”

Merz knows the stakes, not least after a poll by Forsa released last week showing the AfD winning 24% of the vote — just one point behind his bloc. His awareness of the moment was clear in his announcement, even featuring former European Central Bank chief Mario Draghi’s saving-the-euro “whatever it takes” language.

“If this government can’t make it happen now…,” said Gatzer, trailing off as he pondered the rise of the AfD.

—With assistance from Alessandra Migliaccio, Alexander Weber, Arne Delfs, Iain Rogers, Michael Nienaber and Petra Sorge.

Article content